Retirement Planning

Know your retirement date.

With math, not hope.

10,000 Monte Carlo paths over your real accounts. Eight withdrawal strategies, couples modeling, Roth conversion ladders, and tax math for every US state plus DC, and for Ontario, BC, and Alberta.

14 days free · Full Pro access · No credit card

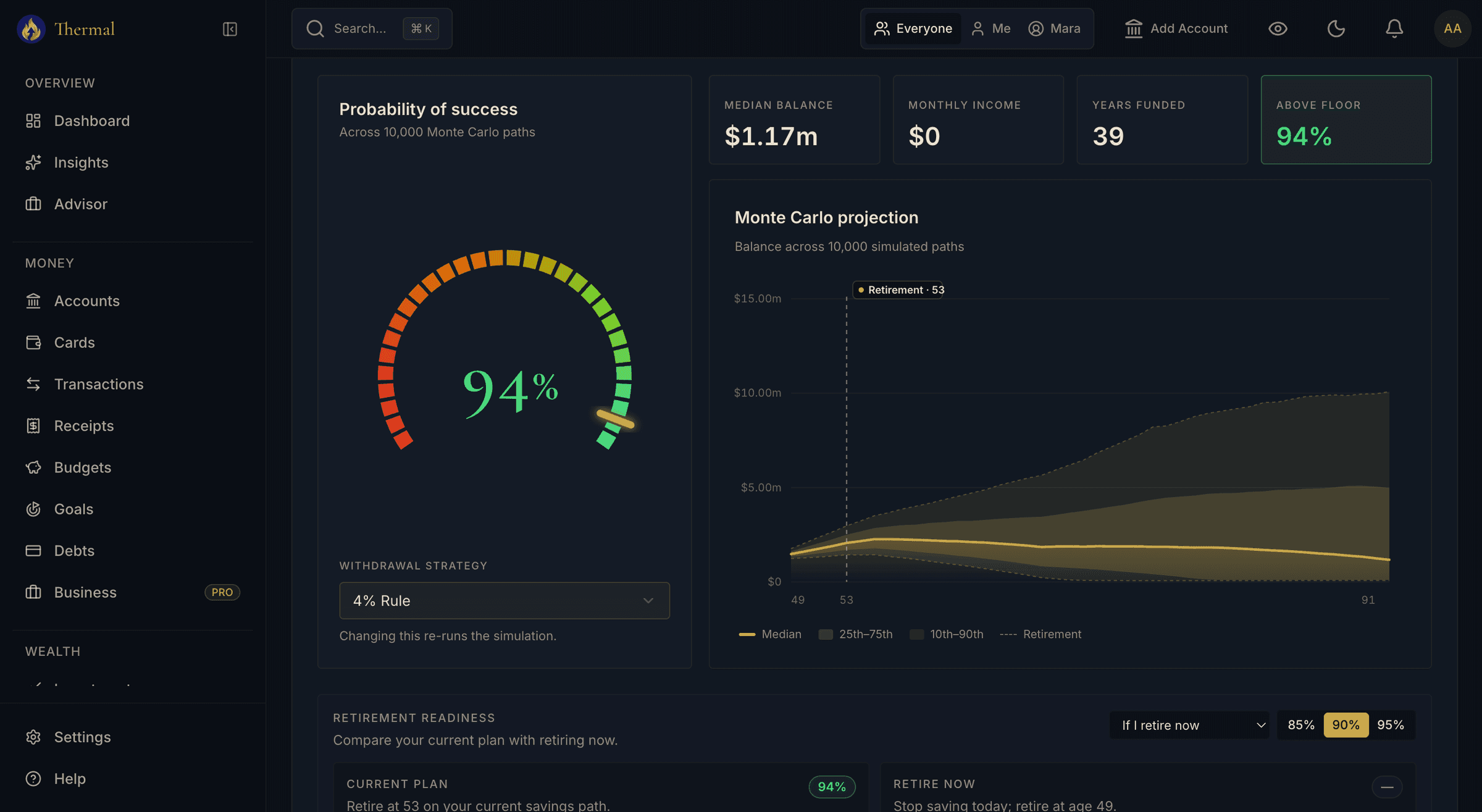

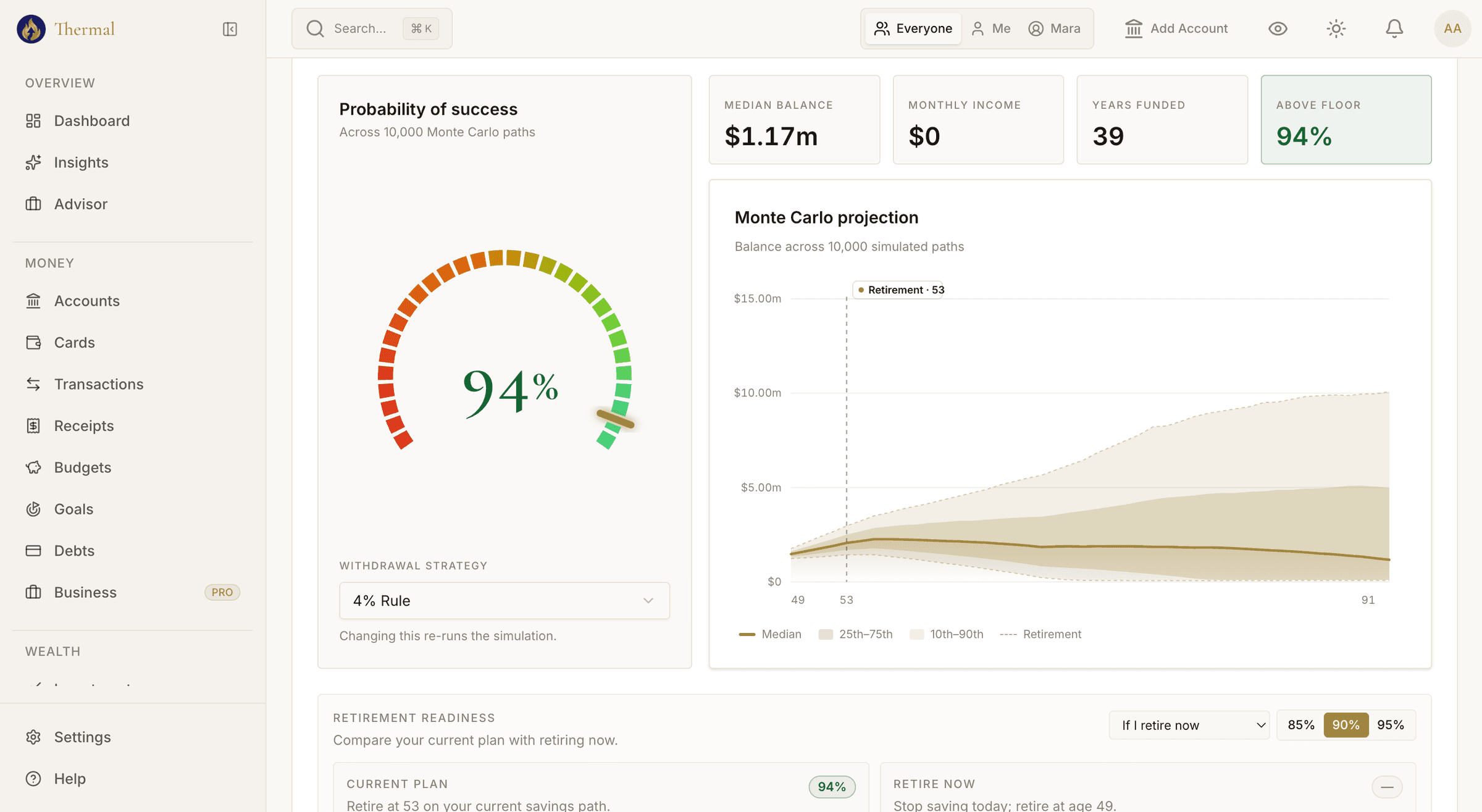

Change the withdrawal strategy and the simulation re-runs on the spot.

How It Works

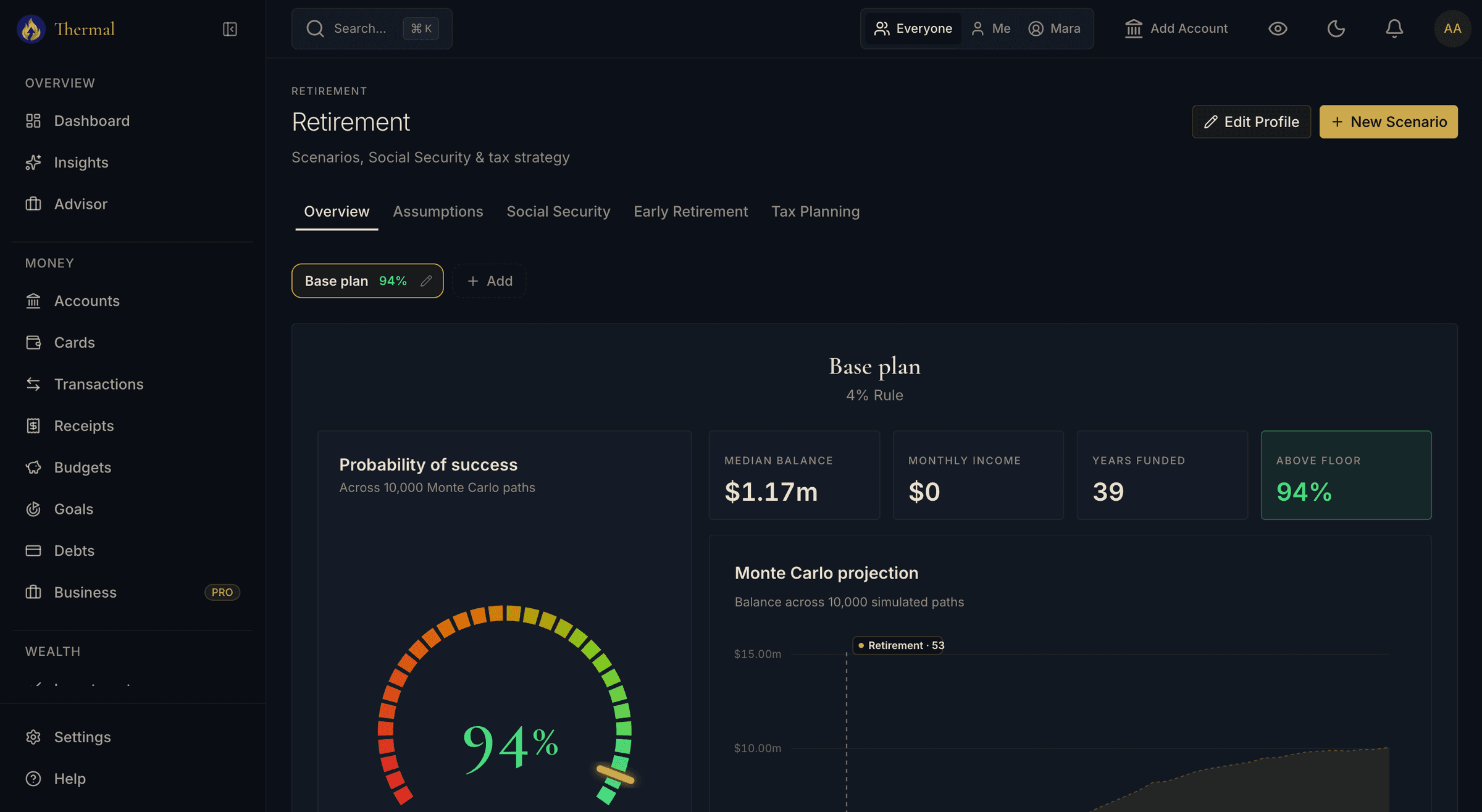

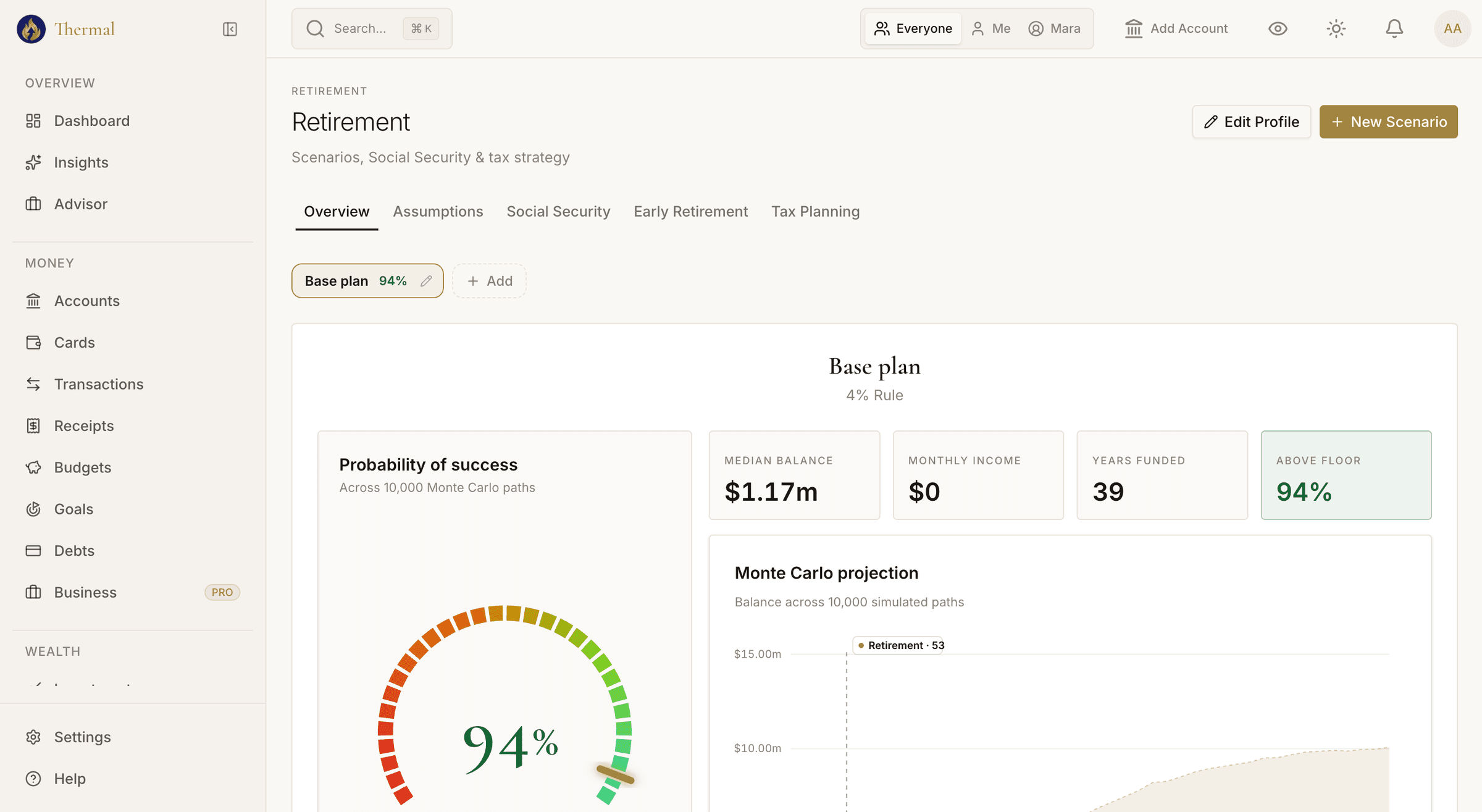

10,000 possible futures, one clear answer

Monte Carlo simulation doesn't predict the market. It models thousands of plausible outcomes so you can plan for uncertainty instead of pretending it doesn't exist.

Step 01

Start from your real accounts

Thermal pre-fills the plan from your linked taxable, pre-tax, Roth, HSA, and optional 529 accounts. Adjust contributions, returns, inflation, and retirement age from there.

Step 02

Run 10,000 simulations

Each path randomizes market returns from historical distributions and walks your plan year by year: contributions, withdrawals, RMDs, and taxes.

Step 03

Get a number you can act on

A success rate, a spending-floor breach rate, and a comparison against retiring right now. If the answer is "not yet," you see which lever moves it.

The Tax Engine

Where most planners round, Thermal computes

Withdrawal order, account type, state of residence, and conversion timing change retirement outcomes by years. The engine treats them as the first-class problems they are.

Federal + 50 states + DC

2026 tax tables for every US jurisdiction, locked down by source-cited regression tests. Your plan is taxed where you actually live, not at a hand-waved flat rate.

Three account buckets

Traditional, Roth, and taxable balances are simulated separately, with four withdrawal orderings: tax-efficient, traditional-first, Roth-first, or pro-rata.

RMDs done right

Required minimum distributions follow SECURE 2.0 age thresholds and come out of traditional accounts only, exactly as the IRS will insist.

Roth conversion ladders

Plan multi-year conversions during low-income years. Thermal models the tax paid now against the tax-free growth later, year by year.

Social Security, your way

Estimated from your income and age by default. Import your full SSA earnings history when you want benefit math to the dollar, and test claiming ages against each other.

Canada, for real

Ontario, BC, and Alberta residents get RRSP, RRIF, and TFSA modeling with provincial tax tables and CAD amounts. Not a US plan with the labels swapped.

Scenarios are side-by-side plans: keep a base plan, then test retiring at 55, a market crash, or a bigger house.

Withdrawal Strategies

Eight strategies. Your retirement, your rules.

The 4% rule is a starting point, not the answer. Pick the strategy that fits how you actually want to live, and see its success rate before you commit.

Guardrails (Guyton-Klinger)

Adjusts withdrawals up or down based on portfolio performance. Spends more in good years, cuts in bad ones. The default, because it works.

4% Rule

The classic: withdraw 4% of your initial portfolio, adjusted for inflation each year. Simple and battle-tested.

Dynamic Percentage

Withdraws a fixed percentage of the current portfolio each year. Naturally adjusts to market conditions.

Variable Percentage Withdrawal

Calculates withdrawals from remaining life expectancy and asset allocation, the Bogleheads way.

Floor and Ceiling

Sets minimum and maximum withdrawal bounds. Guarantees a spending floor while capturing upside.

Endowment

Models university endowment spending rules. Smooths withdrawals across market cycles.

Buy, Borrow, Die

Borrows against the portfolio instead of selling. Models loan mechanics, margin rates, and stepped-up basis.

Custom

Define your own withdrawal schedule year by year. Full control for those who want it.

Real-Life Modeling

Plans fail on the details. Model them.

A 30-year flat spending line is fiction. Thermal models how retirement actually unfolds.

Spending smile

Real retirees spend more at 65 than at 80, then more again late in life. Thermal can curve your spending instead of assuming a flat line for 30 years.

Long-term care

Model a late-life care event: when it might start, what it costs, how long it lasts, and what it does to your success rate.

Cost-of-living adjustments

Income sources carry their own COLA assumptions, so a pension that never adjusts is modeled differently from Social Security.

Couples, modeled honestly

Both partners get their own age, retirement date, income, and Social Security benefit, taxed jointly. One plan for two lives.

14 days free · Full Pro access · No credit card

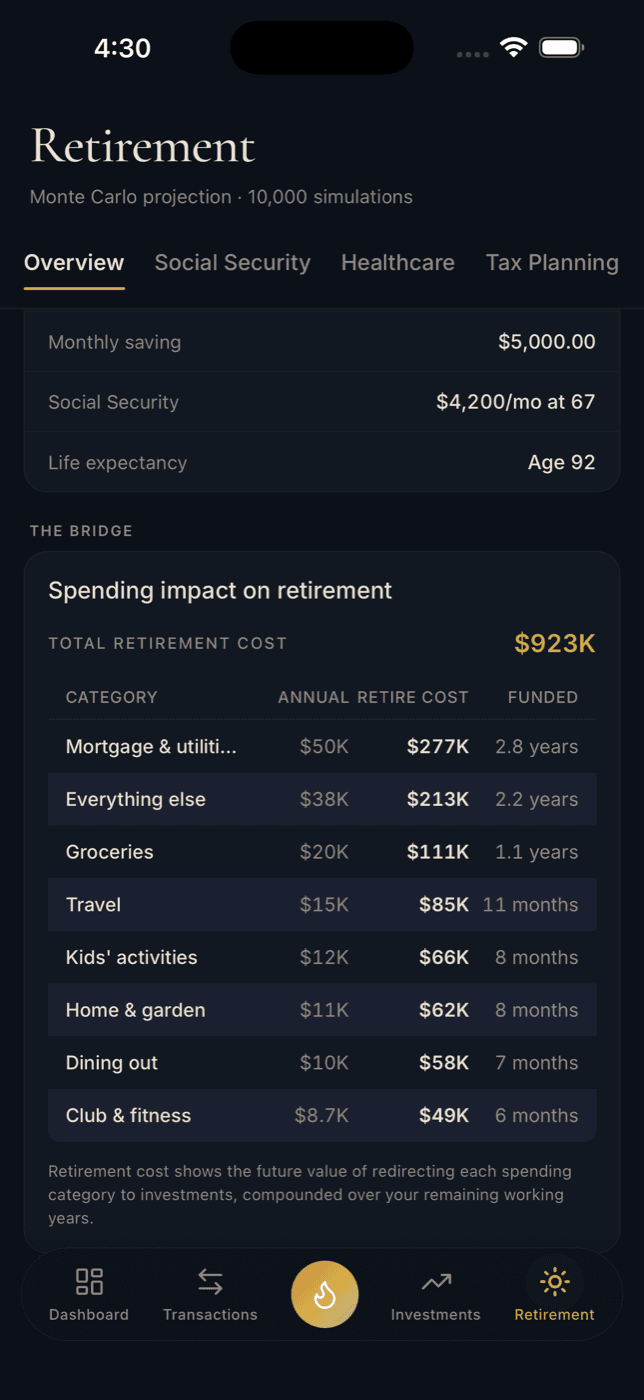

The Bridge

See what today's spending costs your retirement

Most apps treat budgeting and retirement as separate problems. The Bridge connects them: each spending category is priced as the future value of redirecting it to investments over your remaining working years. Dining out stops being $10K a year and becomes $58K of retirement, or seven months of freedom.

It reads your envelope surplus too, so a month of disciplined budgeting shows up where it matters most.

See envelope budgeting →

Work With Your Advisor

Scenarios your advisor can propose, and you can decline

Give an advisor read-only access and they can draft scenarios against your real numbers. You review each one next to your own plan and accept or decline. Your plan stays yours.

See households & advisors →10,000

simulated paths behind every success rate

Ready to run your first simulation?

Link your accounts, set your assumptions, and see your success rate in under five minutes.

14 days free · Full Pro access · No credit card